*Based on our cost data, received directly from user feedback.

Here's how it works:

It’s important to hire a conveyancing solicitor. If you try to complete your own conveyancing, you run the risk of mistakes being made. Here are a few reasons why hiring a solicitor is crucial:

As they are legal experts, you can rest assured knowing you will have the correct legal protection. All our partners are regulated by either SRA, CLC, LSS, LSNI or CILEx, which means they follow the correct protocols.

Conveyancing solicitors are experts in their field and are equipped to handle the complex legalities involved in conveyancing. This ensures your property transaction is completed correctly.

Your conveyancer will complete all paperwork on your behalf quickly and efficiently. This will save you time not having to do it yourself, and you can rest assured knowing everything is correct.

By hiring a conveyancing solicitor, you don’t have to worry about completing the conveyancing process yourself. They will explain everything in detail and ensure any legal jargon is clear to avoid any confusion.

Really great service from premium property lawyers through my home conveyancing.Sian Peek

Muve were standout professionals, offering clear guidance, invaluable help, and consistent support.Mark Ryan

The service was great and on time.Feyisanmi Adeshina

Good value and communication throughout the process.Frank Roberts

Very good and efficient. Good value.Basat Hussain

Natalie has been very helpful throughout the process. Quick to respond and no lawyer speak.Rhiannon Wheeler

Efficient and reasonably priced.Tessa Sheridan

Conveyancing describes the legal process of transferring ownership of a property. This includes everything from buying and selling a property, and first-time buyers, to remortgaging and the transfer of equity.

So what is a conveyancer? A conveyancing solicitor is experienced in the legal aspects of the transaction. Here is what you can expect from the conveyancing process:

1. Hire and instruct a conveyancing solicitor – You must provide all the details for your property and confirm you’re happy to proceed.

2. Conveyancing searches and drafting contracts – Your conveyancer will conduct conveyancing searches and create a draft contract.

3. Exchange of contracts – Once all parties are happy with the contracts, they are exchanged, and a completion date is set.

4. Completion day – On completion day, the legal transfer of the property ownership is complete, and the buyer can move into the property. Check out our Completion Day Checklist.

5. Post-completion – After completion, they will register the property in your name with the Land Registry and pay any Stamp Duty Land Tax.

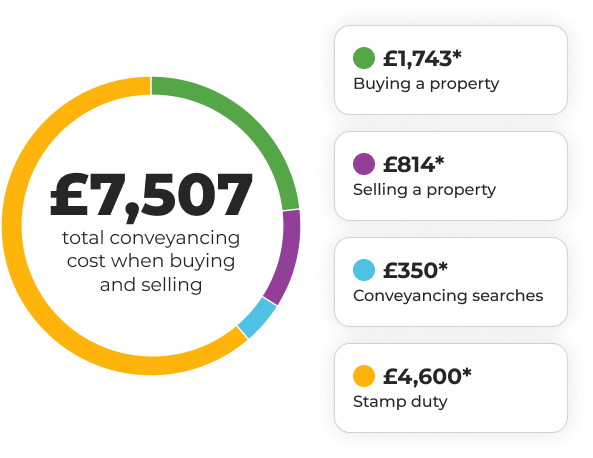

The average conveyancing fees in the UK are £1,624 for buying and £1,023 for selling*. Solicitor’s fees are usually fixed or based on your property’s price, but they can vary depending on whether it’s freehold or leasehold.

Your overall conveyancing fees will consist of the solicitor’s legal fee and conveyancing disbursements. Disbursements are third-party costs that your solicitor will pay on your behalf. Disbursements are unavoidable third-party costs (like searches, processing a TR1 form, and Stamp Duty) that your solicitor pays on your behalf.

Some disbursements are fixed, such as Land Registry fees and ID checks, while others vary depending on your circumstances, such as transfer of equity and leasehold disbursements.

Check out our conveyancing calculator as well as our lease extension calculator for detailed quotes.

*Based on the average service costs for Compare My Move users. See how our data works.

After making an offer on a house and once an offer is accepted, conveyancing usually takes between 8 to 12 weeks, from acceptance to completion. Compare My Move connects you with competent and proactive professionals who can help speed things up they are solicitors for buying a house or solicitors for selling a house.

Specific times will vary depending on the complexity of the property transaction, your solicitor, and whether the home is leasehold. Necessary documentation, such as the deed of variation, can delay the process as it can take longer to acquire.

The length of the property chain is also a factor to consider. The longer the chain, the more likely delays are due to there being more paperwork and steps involved.

Both conveyancers and solicitors can handle the legal work involved in property transactions, but they differ in focus, cost, and scope:

Whichever route you choose, regulation is key. All our partners are fully regulated by the SRA, CLC, or an equivalent body, so you can compare quotes with confidence.

Explore our expertly-reviewed guides on conveyancing and more.

What Is a Conveyancer?

What Is a Conveyancer?

Conveyancing Fees in 2026: How Much Does Conveyancing Cost?

Conveyancing Fees in 2026: How Much Does Conveyancing Cost?

What are Conveyancing Disbursements?

What are Conveyancing Disbursements?

How Long Does Conveyancing Take?

How Long Does Conveyancing Take?